The IFRS 17 Risk Adjustment creates challenges for (re)insurers, such as how to determine the confidence level needed for disclosure purposes, and how to restate a given confidence level over different time horizons. This paper presents a solution to address these challenges and details a case study for a life company.

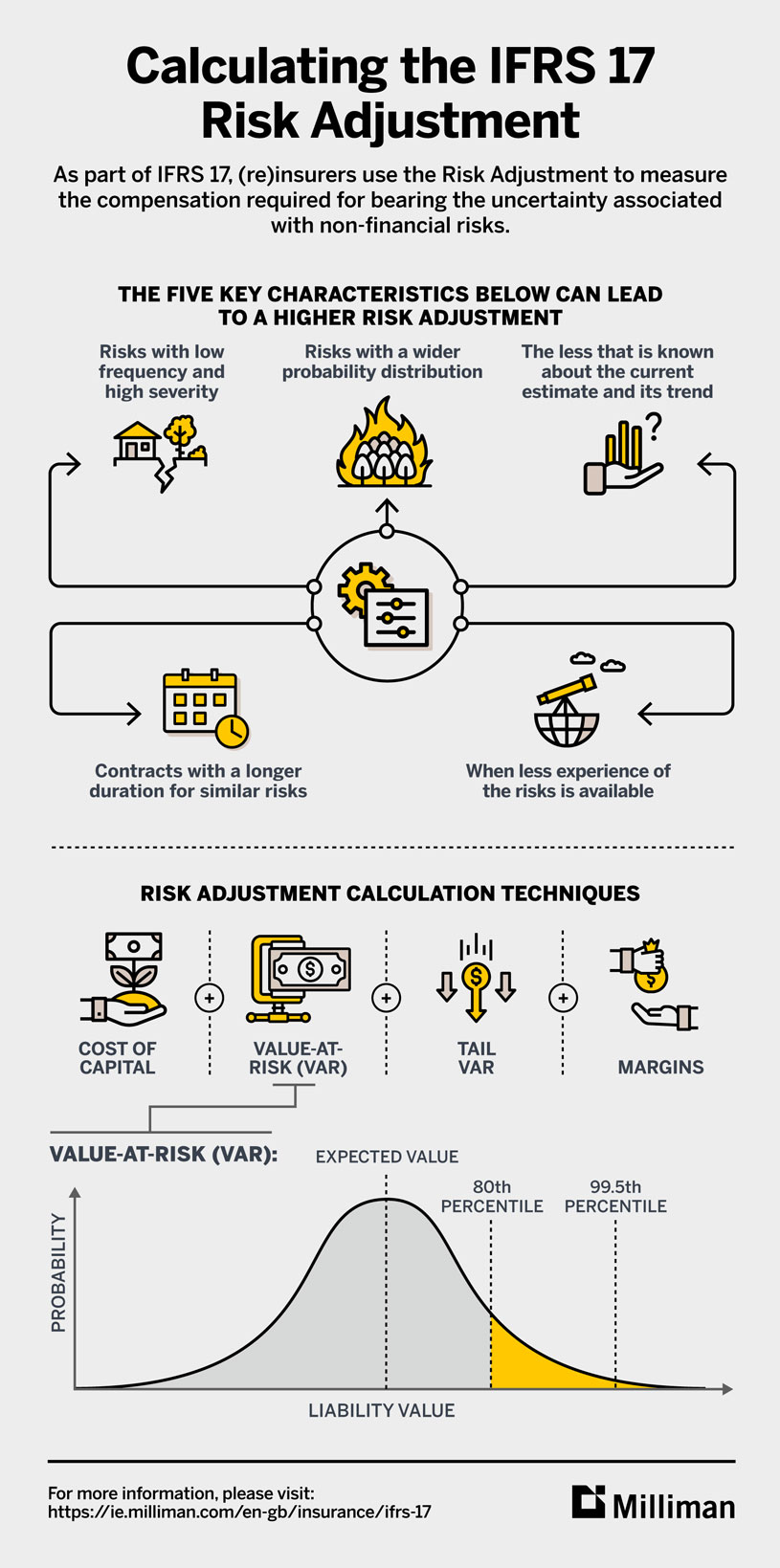

Below is an infographic that highlights the five key characteristics that can lead to a higher risk adjustment and the risk adjustment calculation techniques.