The House Ways and Means Committee in H.R 2954 passed the Securing a Strong Retirement Act (SECURE Act 2.0) on May 5, 2021, which is currently awaiting further approval in Congress. It gives employers the option to match their employees’ student loan payments to a lender, holding the loan with the employer’s contributions to a defined contribution plan under IRC §401(m). The proposal includes the incentive to adopt such a provision with a regulatory safe-harbor that provides exemption from “non-discrimination testing” requirements.

For the sake of this discussion, we will refer to such potential employer matching contributions as Student Loan Matches or SLiMs©. Whether the SECURE Act 2.0 becomes new law or not, debates over student loans and how they should be addressed have been a recurring theme in proposed legislation over the past years (e.g. the proposed Heroes Act–H.R. 6800 in May 2020) that is likely to continue until relief is provided. In June 2021, Senators Ben Cardin and Rob Portman introduced a similar SLiM provision in S. 1770, which the Senate has yet to review.

This leaves employers with three questions:

- Is student loan debt a problem?

- How could a SLiM to a defined contribution plan mitigate the problem for the members of an employer’s workforce who have student loans?

- If a SLiM becomes a statutory option for an employer to adopt, is it worth considering?

This article provides background information for each of these questions and pertinent considerations in the quest for answers.

Is student loan debt a problem?

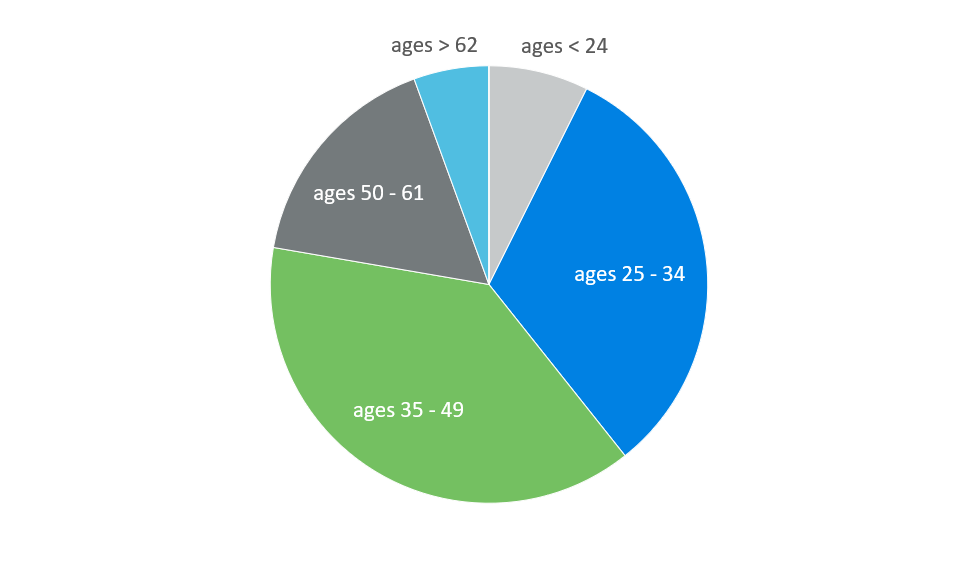

As of 2021, 45 million individuals in the U.S. carry student loan debts equal to a total of $1.7 billion, surpassing auto loans and credit card debt, and second only to mortgages. The average loan carried by a student graduating in 2021 is $37,693, an increase of 15% from 2020.1 The debt load is a multi-generational reality. CNBC published a report in December 2020 that provides the following data.2

Percent of total student debt by age group

Why are legislators addressing student loans as a concern in the context of retirement security?

Financial volatility ranks third in the top current risks, according to a January 2021 survey by the Society of Actuaries.3 The key to saving for sufficient retirement income is to start saving early in life and save consistently to benefit from compounding growth of long-term investments. This is becoming increasingly difficult for workers to achieve.4 Student loan debt seriously compromises how committed people are to making that happen because as long as workers have any debt, they tend not to save for retirement. Just the “mere presence of debt weighs on people,” says Geoff Sanzenbacher, associate research director for the Center for Retirement Research at Boston College. “They don’t save much no matter how much debt they have. That is a little bit surprising.”5 If student loans are keeping millions of individuals from saving for retirement, they are a threat to retirement security. And that is a problem.

How could a SLiM address the problem?

SLiMs do not reduce the burden of student loans, but they reduce the negative side-effects for individuals. Instead of postponing all savings for retirement until after student loans are paid off, it makes it possible for retirement savings to start as soon as an employee is eligible to participate in a plan.

SLiMs do not reduce the burden of student loans, but they reduce the negative side-effects for individuals.

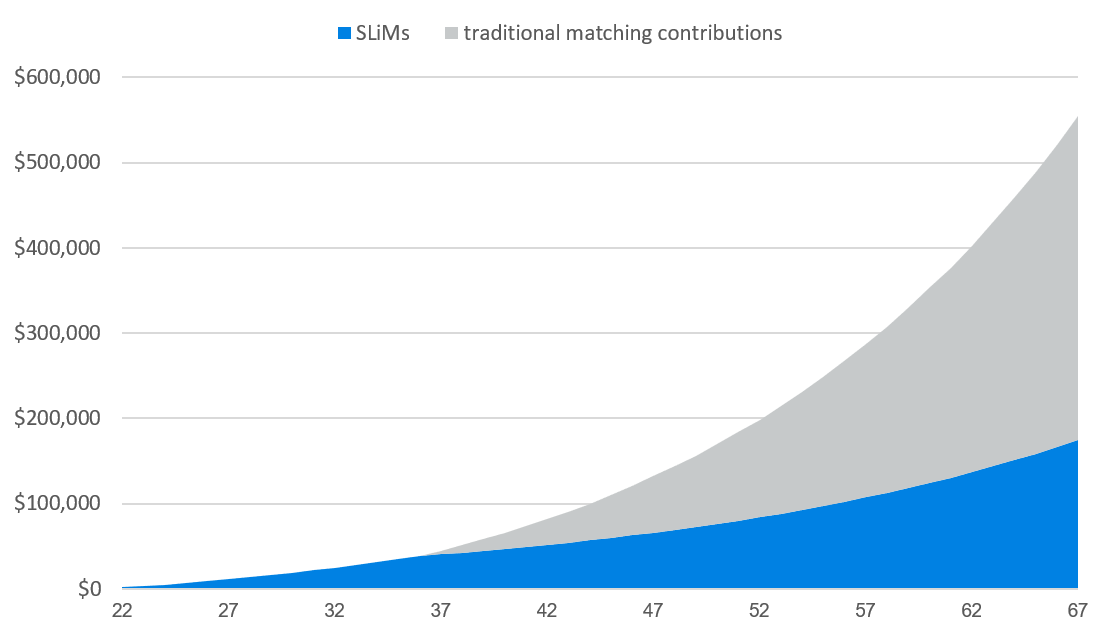

To better capture the potential ramifications, let us consider an example for a particular graduate who starts a job for an employer with a qualified savings plan. We will make the following assumptions:

- Starting salary at age 22 of $50,0006

- 2% annual salary increases

- 3% employer match

- 15-year loan payment duration

- 3% employee contribution after loan paid off

- 5% investment return for all years

This scenario is summarized in the graph below.

Growth of SLiMs made before employee match

With the individual never contributing more than the 3% needed to receive the employer match portion, the percentage of savings at retirement that are attributable to the employer contributions while student loans are being paid off (in light blue) accounts for nearly one third of final savings at retirement. If the individual were to make contributions at a higher rate, that final percentage would be lower. However, this example demonstrates that even relatively small contributions in the early years of a working lifetime can have a big impact on retirement readiness when that time comes.

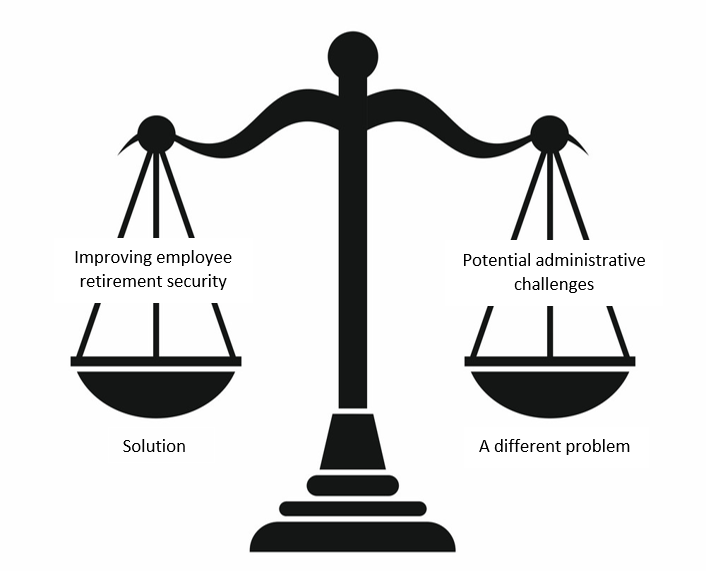

If it becomes an option, is this benefit worth implementing?

To answer this question, we need to ask a few more. Who are the employees? How essential is a secondary education degree to the employer for delivering products and services? What percentage of the employee population has student loans? What is the critical mass of employees with student loans to make adopting a SLiM worthwhile? If it’s deemed to be a valuable benefit, what are some administrative challenges? How might one overcome these challenges?

First, an employer needs to evaluate the employee population to determine how beneficial the non-traditional employer matching contributions might be. What percentage of the employee population is college educated or has other advanced degrees? Using a prudently crafted anonymous survey (so as not to violate privacy laws), an employer may want to survey workers to determine what percent are carrying college loans and approximately how much. The results of such a survey can then be weighed in the balance of pros and cons. What percentage of employees with student loans is desirable for non-traditional employer matching contributions to be worth the implementation? 10%? 40%? 70%? There is no correct answer, just the best answer for a particular employer and the employees.

Second, if it is determined to be the best decision, what are the administrative tasks and internal governance needed to affect adoption of a SLiM? Initially, there would be a need for a formal savings plan amendment. Next, a mechanism (preferably automated) would have to be put in place for confirming that the loan holder received a student loan payment before the employer would make the SLiM. The loan holder’s frequency of such attestation would also need to be considered.

Coordinating such efforts with the employer’s payroll provider might become an option. Senator Lamar Alexander in the Student Loan Repayment and FAFSA Simplification Act S. 4247 on July 21, 2020 proposed making student loan payments directly out of payroll. It would behoove the employer to set up loan payment verification in a manner that includes a secondary confirmation to avoid any fraudulent claims of a loan being paid.

Another option would be to make employer contributions annually, based on an end of year confirmation of total student loan payments plus any salary deferrals made directly to the plan. Companies could possibly match on salary deferrals throughout the year and perform an annual true-up of match when also considering student loan payments based on an end of year confirmation of total student loan payments. While a one-time, end-of-year confirmation would be easier to manage, it might create a loss of investment income on new contributions as for a true-up of match.

Conclusion

Employee benefits are a critical element of how employers define themselves and set them selves apart from other employers for attracting talent and retaining experienced employees. Younger workers place a higher value on employer benefits than previous generations did; they have been shown to value them even more than salary treatment. In fact, student loan repayment benefits rank third amongst their most desired benefits.7

If employers consider the value they place on supporting younger employees to achieve retirement readiness, and assess the administrative challenges that will come with non-traditional employer matching retirement contributions, they will be ready for opportunities to address the needs of their employees. Is a solution for improving retirement security worth the potential administrative challenges of implementation? Employers will be faced with such a decision if SLiMs become part of retirement law.

1Zach Friedman. (February 20, 2021). Student Loan Debt Statistics in 2021: A record $1.7 Trillion. Forbes.

2Megan DeMatteo. (December 12, 2020). Here’s the average student loan debt by age. CNBC.

3Max J. Rudolph. (January 2021). 14th Annual Survey of Emerging Risks. Society of Actuaries.

4Paula Aven Gladych. (July 12, 2018). Do young adults with student loan debt save less for retirement? EBN BenefitNews.com.

5Dan Doonan and Tyler Bond. (September 2020). The Growing Burden of Retirement: Rising Costs and More Risk Increase Uncertainty. National Institute on Retirement Security.

6Average for college graduates based on Summer 2020 Salary Survey. National Association of Colleges and Employers.

7Stephen Miller. (June 5, 2019). Younger Workers Put Student Loan Aid Near Top of Desired Benefits. Certified Employee Benefit Specialist.