Federal Reserve Chair Jerome Powell announced several rate hikes in 2022 to combat inflation and to stabilize prices. Almost two years later, with a strong economy and falling inflation targeted at 2%, it is expected that we will see rate cuts begin in 2024.

For many companies with defined benefit (DB) plans, the 2022-2023 rate hikes resulted in an improvement in the funded status of their corporate pension plans. We saw an increase in de-risking initiatives and standard plan terminations that had been put on hold for many years waiting for rates to rise. Some plan sponsors, including IBM, decided to use the overfunding to reopen their frozen plans to provide retirement security to employees through a DB plan replacing their hard-dollar defined contribution (DC) match.

With the possibility of rates decreasing in 2024, there are a few things that plan sponsors can do to navigate through the change. Depending on plan demographics, a 100bps decrease in rates could increase pension plan liabilities anywhere from 8% to 15%. In this article we discuss tools, strategies and resources to help plan sponsors proactively manage their DB plans in order to prevent any significant deterioration of the recently improved funded positions.

Six ways for pension plan sponsors to prepare for interest rate cuts

What do DB plan sponsors need to do to prepare? Below is a list of key things to consider:

1. Lock in funded positions

With the improvement in funded positions resulting from high interest rates, now may be a time to explore securing the funded position with more immunized investing. Asset liability management (ALM) allows plan sponsors to coordinate investments with plan liabilities to achieve desired financial goals. Liability-driven investing (LDI) is an application of ALM that emphasizes reducing the volatility of a plan’s funded status and contribution requirements. This means not only matching existing fixed income duration to the timing of expected plan distributions, but potentially increasing the fixed income matched allocation of the plan assets as funded status improves. The matched investments and liabilities move in tandem and the net funded status stays relatively consistent from year to year for this portion of the portfolio. Many plan sponsors consider a glide path (see Figure 1) as they shift their current investment strategies to an LDI approach. The glide path may vary depending on the plan sponsor’s overall risk tolerance and the accrual status of the plan (frozen vs. ongoing).

Figure 1: Glide path

| Funded Status | Return Seeking | Liability Hedging |

|---|---|---|

| 80% | 45% | 55% |

| 85% | 40% | 60% |

| 90% | 35% | 65% |

| 95% | 30% | 70% |

| 100% | 25% | 75% |

| 105% | 20% | 80% |

| 110% | 15% | 85% |

| 115% | 10% | 90% |

| 120% | 5% | 95% |

Securing this funded position may cause some unintended consequences. A holistic review is recommended before making any significant change to the investment policy. For example, more fixed income may require a modification to the contribution policy to make up for lower return expectations on the assets and/or result in an increase in the Financial Accounting Standards Board (FASB) pension expense report on the profit and loss (P&L) statement.

2. Transfer risk via lump sums

With rates still at levels not seen since 2011, de-risking remains a cost-effective option. It reduces the plan footprint so future volatility may not be as significant to the sponsor’s overall financial position. Some de-risking initiatives, like lump sum windows, can use 2023 rates for transfers in 2024. These initiatives not only shrink the size of the plan, but they can also potentially reduce Pension Benefit Guaranty Corporation (PBGC) premiums by over $700 per participant annually. Similar to locking in the funded position, a risk transfer can impact other aspects of the plan and should be fully vetted. A lump sum sweep analyzer tool will validate the cost benefit analysis and provide insights into the cash, accounting and PBGC savings; allowing plan sponsors to find an optimal time to consider such windows.

3. Consider a contribution policy above the minimum required amounts

With or without de-risking via ALM or a transfer of risk, reviewing the contribution policy in light of potential market changes to identify any need for cash contributions is key. Avoiding unexpected cash requirements is a crucial part of managing risk. There are a multitude of reasons for plan sponsors to consider contributing an amount above the minimum required contribution. Excess contributions can decrease the variable rate portion of PBGC premiums (currently capped at 5.2% of underfunded status), allow flexibility for future contribution requirements and help with budgeting, be tax-deductible, and improve future funded status with accumulated return. Creating a cushion with a stable funding policy is a great way to minimize the volatility that can be seen in year-to-year cash requirements based on the results of the annual actuarial valuation.

4. Potential PBGC premium options

If decreasing rates result in an increased underfunded position, estimating the effect on the PBGC variable rate portion of the insurance premium may be prudent. The good news is that a 2024 rate decrease will not affect premiums due until 2025, so for this topic we have some time. That being said, there are two methods for determining the variable premium amount. A sponsor can change methods once every five years with automatic approval. If there is an anticipated increase in the premium due in 2025 as a result of a decrease in 2024 rates, then it may be worth reviewing the impact of a switch in methods. If a switch doesn’t make sense, having time to plan for an increase is still valuable. Another option to decrease PBGC premiums is to complete a pension risk transfer of a subset of the retiree population. Selecting the appropriate subset can help the plan sponsor save on PBGC premiums, without crossing the settlement accounting threshold or impacting the minimum required contribution. Similar to a lump sum sweep, reducing the participant count can reduce the PBGC by $700 per participant annually as well as other administrative costs. As mentioned above, additional contributions can also decrease the PBGC variable rate premium.

5. Prepare for workforce management needs

Offsetting effects on a sponsor’s workforce may occur as rates decrease. Employees with an additional 401(k)-type retirement plan could see an increase in the value of their savings, and decide to leave employment earlier than expected (especially if they are invested in fixed income when rates drop). However, the potential recession that could result from rate cuts and a slower economy may cause an offsetting pause to those with imminent retirement plans. These changes can also affect payroll costs, training resources, and employee/institutional knowledge. Being able to plan and prepare for your future hiring needs is an integral part of successfully operating your business.

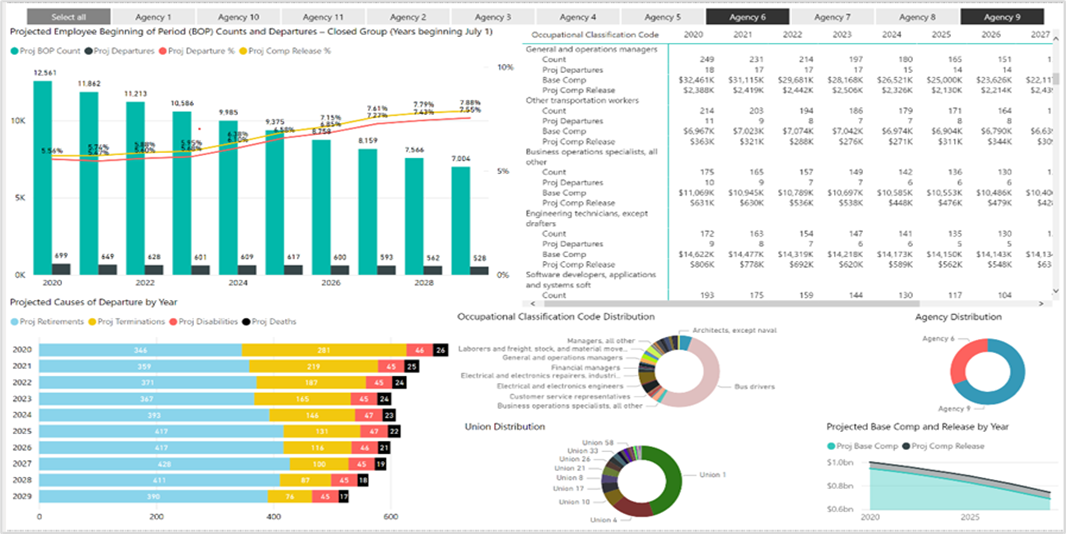

Assessing anticipated impacts of workforce changes with forward-looking tools and scenarios like the one shown in Figure 2 can help employers be better prepared to mitigate unfavorable change. This interactive platform allows employers to understand actuarially projected changes in workforce demographics to assist in understanding the hiring needs of various departments and locations at a granular level. By using a tool like this, employers can be proactive in succession planning throughout their organization. The data can be sliced and examined by job code, union, job classification, location, etc.

Figure 2: Workforce management planning analysis

6. Consider alternate plan designs

For sponsors with DB plans that have final average pay designs (a percentage of final average pay times years of service), now may be a good time to explore alternative plan designs. Hybrid plans have gained a lot of popularity, and for good reason. They can reduce volatility and pension plan footprint while still achieving employer attraction and retention goals. They can often be a low-cost alternative to a defined contribution plan, and they are understood and appreciated by a young and mobile workforce. In traditional defined benefit plans, the plan sponsor bears the interest rate risk, the investment risk, and the longevity risk. Similarly, in a defined contribution plan, the employee bears those risks. Moving to a hybrid plan design allows these risks to be shared between the plan sponsor and participant. A hybrid design can be tailored to match the risk tolerance of plan sponsors.

Another cost control design consideration is the removal of ancillary benefits. Altering provisions such as death benefits over the minimum required by law or cost of living adjustments can help reduce plan liability. Thoughtful consideration of the plan population and goals should be taken into account when making any plan change.

Conclusion

Although the anticipated decrease in rates is not expected to be as sharp or to occur as fast as the increase in rates experienced in 2022, DB plan sponsors should be informed and prepared. In today’s environment, surprises are generally not welcomed. Having a plan to address any potential challenges keeps plan sponsors one step ahead of the changes and helps them prudently manage their retirement programs. Milliman actuaries have the expertise and tools to help you proactively stay ahead of the curve in managing future risk and optimizing your retirement benefit solutions.