Retiree Health Cost Index: The 2024 cost of healthcare in retirement

Milliman’s Retiree Health Cost Index (RHCI) is the amount of savings (net of taxes) needed at age 65 to pay for a retiree’s remaining lifetime healthcare costs, assuming an investment return of 3.0% per year. The RHCI was established in 2022, with the goal of providing a market-leading, useful benchmark for recent and future retirees and their retirement planners.

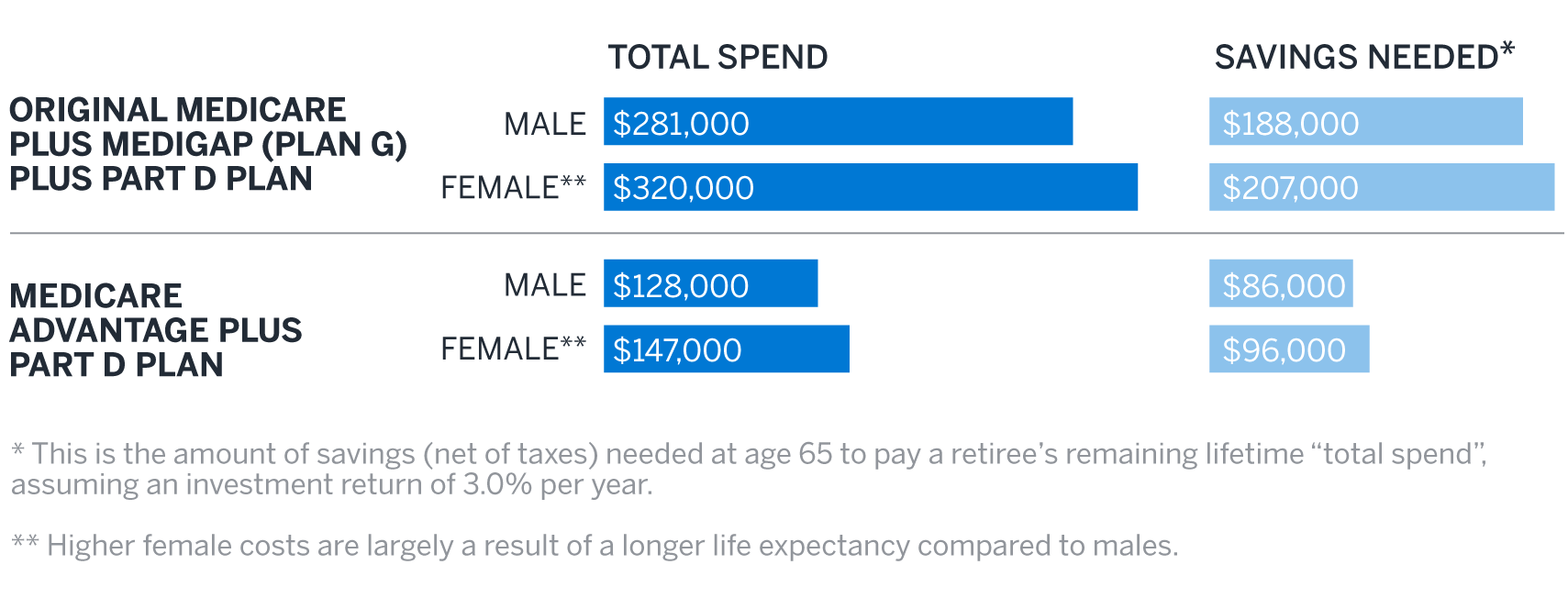

An average 65-year-old retiring in 2024 is projected to spend a substantial amount for healthcare over the course of their remaining lifetime. Figure 1 shows the expected cost for both a male and female retiree under two typical coverage options.

Figure 1: Projected remaining lifetime healthcare expenses for a healthy 65-year-old retiring in 2024

For retirees, it is important to keep in mind that just how much you will pay in retirement may vary substantially from the average amounts in Figure 1 and is dependent on your individual circumstances. There are factors you can control such as when you retire, where you live during retirement, or what benefit plan you choose. You will have less control over factors such as your health status or how long you will live, both of which are primary drivers of how much your healthcare will cost. The costs for the average retiree presented in Figure 1 are a helpful starting point, but you must consider all these factors and more to ensure you are financially prepared to address your healthcare needs during retirement.

How have healthcare costs for retirees changed in 2024?

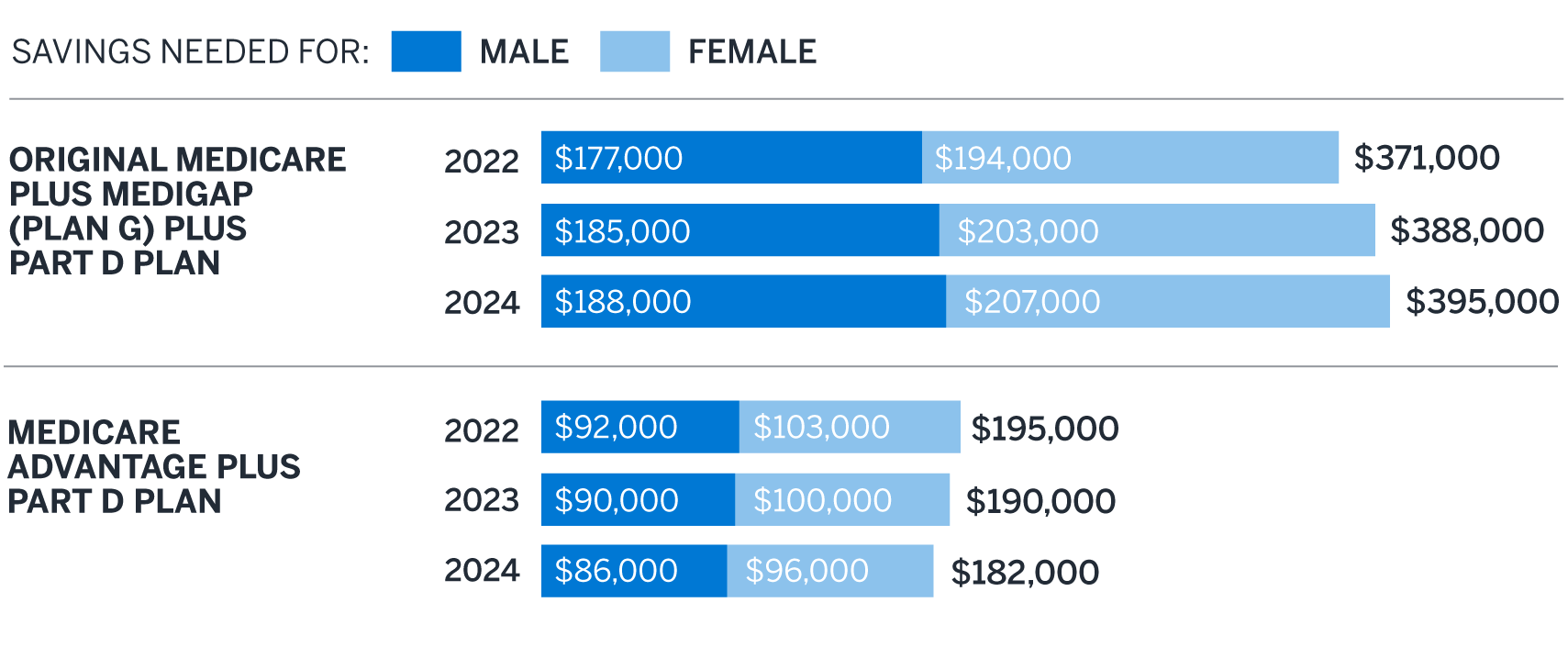

Figure 2 compares the savings needed for a 65-year-old couple1 retiring in 2024 to our estimates from the previous two years. Relative to our 2023 estimates, we project our hypothetical couple retiring in 2024 will need to save approximately $7,000 more if they have Original Medicare plus Medigap and Part D coverage, and $8,000 less if they have Medicare Advantage plus Part D coverage, all else being equal.

Figure 2: Savings needed for a healthy 65-year-old couple retiring, by year

Drivers of change

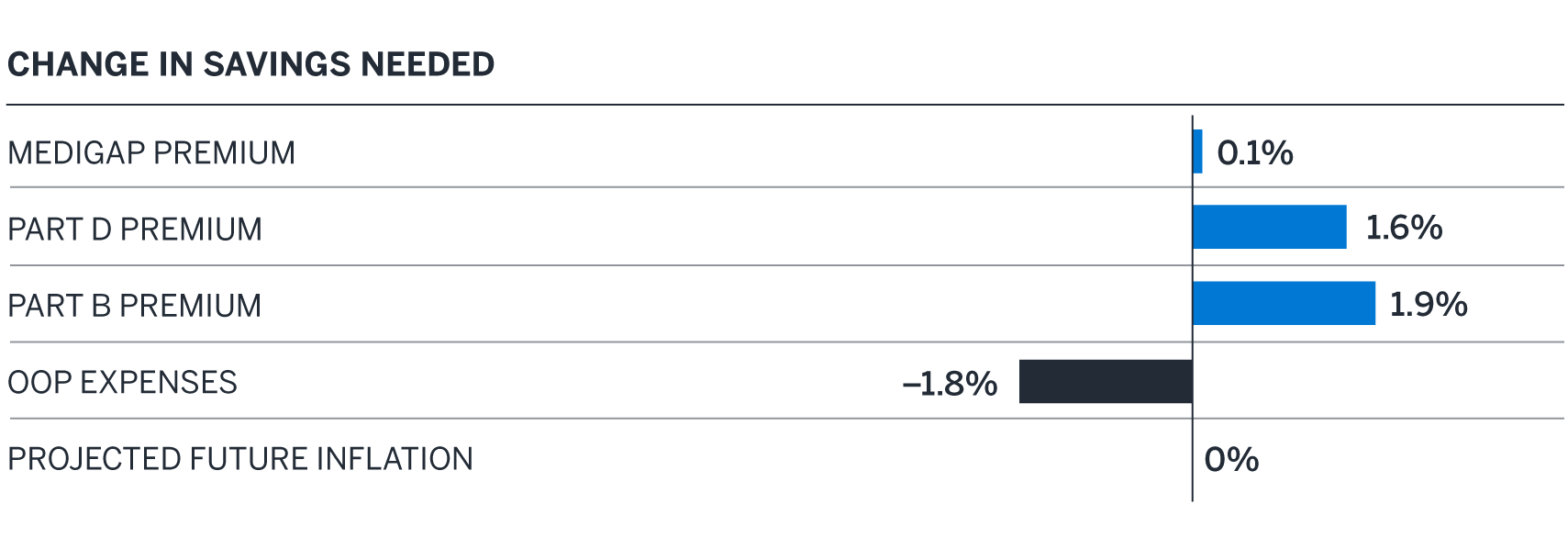

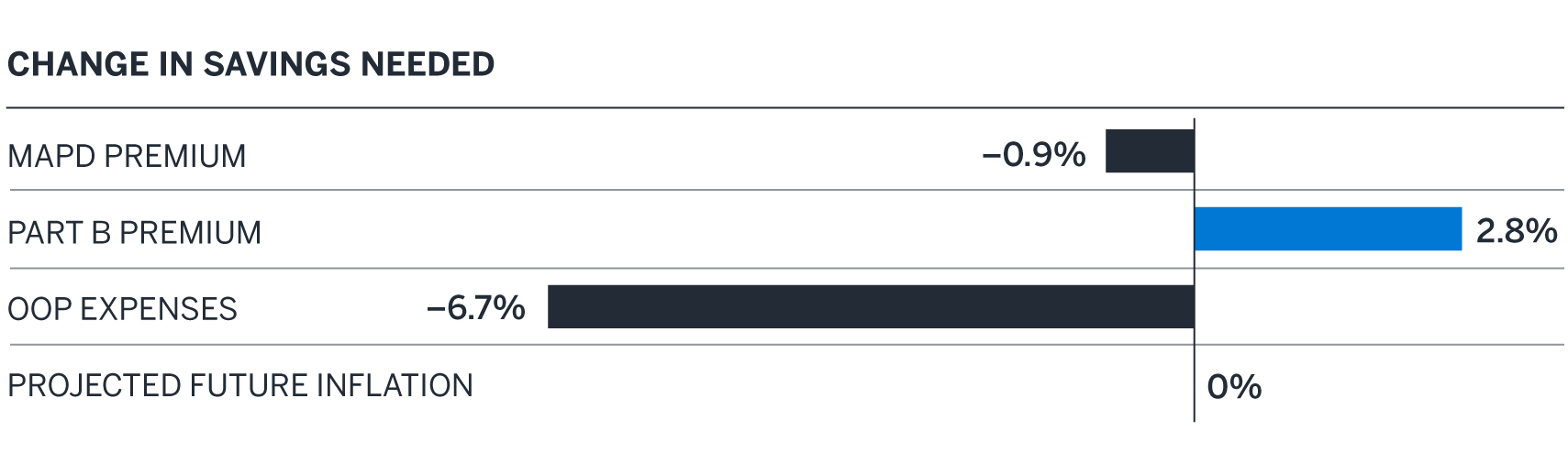

Figures 3 and 4 show the change in overall savings to fund healthcare costs relative to our 2023 estimates, broken down by various components.

Figure 3: 2023 to 2024 changes by component – original Medicare plus Medigap Plan G plus Part D

In particular, we observed the following:

Medigap premium. The premium increase reflects an overall cost trend in the Medicare population, including changes in Original Medicare cost sharing covered by Medicare Supplement carriers offering Plan G, which is largely offset by a decrease in the assumed administrative costs as a percentage of premium.

Medicare Part D premium and out-of-pocket (OOP) expenses. There were significant changes to Medicare Part D in 2024 as a result of the Inflation Reduction Act (IRA).2 Part D OOP expenses were significantly reduced as a result of the IRA’s elimination of cost sharing in the catastrophic phase. However, this change increased the plan liability, driving an increase in premiums. In addition, there has been continued growth in spending on major brand drugs including GLP-1s (even when only covered for diabetes and not obesity), SGLT2s, and certain autoimmune drugs, driving up premium and OOP costs as well as expected trend over the next couple of years.

Medicare Part B premium and OOP expenses. The Medicare Part B premium and deductible are higher, largely due to increases in projected health care spending, per the Centers for Medicare and Medicaid Services (CMS).3

Projected future inflation. Short-term healthcare trend cost expectations over the next couple of years have increased compared to last year, largely driven by higher prescription drug costs. This is offset by decreases in expected medium- to long-term trends such that there is no anticipated change in savings needed under this scenario’s 25-year planning horizon as a result of changes in inflation.

Figure 4: 2023 to 2024 changes by component – Medicare Advantage plus Part D (MAPD)

MAPD premium and OOP expenses. Improvements in the Medicare Advantage program and increased market competition are the main drivers of lower premiums. Lower premiums and improved benefits available in low-premium plans have led members to enroll in lower-premium plans year over year. In general, market competition has fostered creative benefit designs and rich benefit plan offerings. MAPD OOP expenses decreased, driven largely by the IRA changes noted above as well as an increase in the valuation of certain key supplemental benefits that are often included in MA plans.

Changes in Medicare Part B premiums and projected future inflation under the MAPD pathway are similar to those previously described under the Medigap pathway.

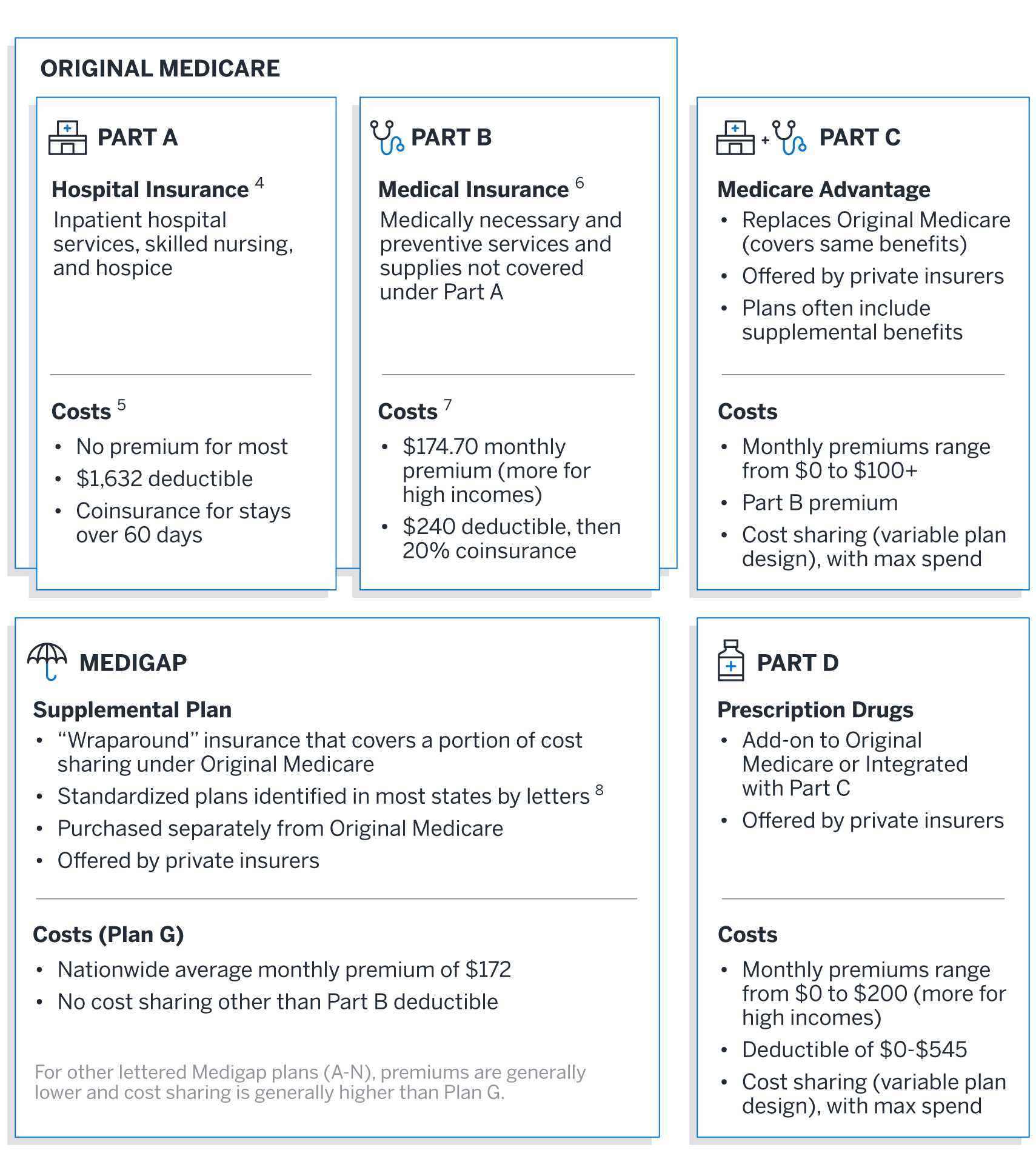

What coverage options do Medicare-eligible retirees have?

Most retirees are eligible for Medicare at age 65 (or earlier, in some cases). Figure 5 gives a brief overview of the medical and prescription drug coverage options available to retirees through Medicare.

Medicare coverage options and costs

We review costs under the two most common pathways taken by Medicare-eligible retirees:

- Original Medicare plus Medigap plus Part D

- We assume Medigap Plan G, as it is the most popular plan for new enrollees

- We assume the 2024 Part D standard benefit design9

- Medicare Advantage plus Part D (MAPD)

- We assume an enrollment-weighted average premium and out-of-pocket cost across all MAPD plans10 (i.e., not limited to a specific plan design)

Although the majority of Medicare beneficiaries obtain healthcare coverage under either Medigap or Medicare Advantage,11 we acknowledge retirees may have other coverage such as employer-sponsored coverage, Medicaid, or Veterans Affairs healthcare that would likely reduce their exposure to healthcare costs during retirement. Retirees may also choose not to add any supplemental coverage to Original Medicare, which may increase or decrease overall healthcare spending, depending on utilization.

Original Medicare plus Medigap (Plan G) plus Part D (standard benefit)

A healthy 65-year-old male retiring in 2024 is projected to spend approximately $281,000 on healthcare expenses during his retirement. The retiree is assumed to have a life span of 88 years. To cover these future healthcare expenses in today’s dollars, he needs $188,000 in savings in 2024.

A healthy 65-year-old female retiring in 2024 is projected to spend approximately $320,000 on healthcare expenses during her retirement. The retiree is assumed to have a life span of 90 years. To cover these future healthcare expenses in today’s dollars, she needs $207,000 in savings in 2024.

If the female retiree lives the same number of years as the male (to age 88), she is projected to spend approximately $277,000 ($4,000 less than the male). She needs $185,000 in savings in 2024 to cover these future healthcare expenses in today’s dollars.

Medicare Advantage plus Part D

A healthy 65-year-old male retiring in 2024 is projected to spend approximately $128,000 on healthcare expenses during his retirement. The retiree is assumed to have a life span of 88 years. To cover these future healthcare expenses in today’s dollars, he needs $86,000 in savings in 2024.

A healthy 65-year-old female retiring in 2024 is projected to spend approximately $147,000 on healthcare expenses during her retirement. The retiree is assumed to have a life span of 90 years. To cover these future healthcare expenses in today’s dollars, she needs $96,000 in savings in 2024.

If the female retiree lives the same number of years as the male (to age 88), her costs are projected to be about the same as the male retiree.

Comparing Medigap and Medicare Advantage

Figure 6 highlights some of the key differences between an average Medigap and Medicare Advantage plan.

Figure 6: Medigap vs. Medicare Advantage

| Medigap | Medicare Advantage (MA) | |

|---|---|---|

| Services offered | Same as Original Medicare. | Same as Original Medicare. Often also includes other supplemental benefits (dental, vision, hearing, etc.). |

| Relationship to Original Medicare | “Wraps around” Original Medicare to provide coverage for out-of-pocket (OOP) costs. | Replaces Original Medicare. |

| Part D prescription coverage | Not included. Would need to be purchased separately. | Typically included, referred to as “MAPD” plan. |

| Provider network | Same as Original Medicare. | Typically more limited than Original Medicare. |

| Prior authorization/referrals | Generally no prior authorization or referral required. | May require prior authorization and/or a referral. |

| Premium level | Varies widely based on age, geography, and plan design. Generally higher than MA. | Varies widely based on geography and plan design. Generally lower than Medigap. |

| Out-of-pocket costs | Limited cost sharing provides greater protection against unexpected OOP costs at the expense of higher monthly premiums. | Varies widely, with potentially high limits and a risk of substantial additional costs. Includes a maximum out-of-pocket cost limit. |

While retirees cannot be enrolled in both Medigap and Medicare Advantage at the same time, you may switch between plan types during annual open enrollment periods. Medigap premiums are often “issue-age” and may cost more at ages after 65 if enrolling late or switching from MA. Medigap insurers may also charge more or not offer coverage at all if you are applying for Medigap coverage after an initial six-month enrollment period (starting the first month you have Medicare Part B and are 65 or older), based on a review of your health conditions. MA plans cannot consider your health conditions in determining eligibility to purchase a plan or to charge different premiums.

Choosing which coverage option is right for you will depend on your individual situation. A healthier retiree who values lower premiums over freedom to choose any healthcare provider may prefer Medicare Advantage. A retiree with higher expected healthcare utilization either currently or expected in the future may prefer Medigap. Whatever your situation, it is important to understand the options available to you and their differences so you can make the best decision for both your health and your finances.

Financial impact of retiring earlier or later than age 65

Financial impact of retiring earlier

Most people cannot apply for Medicare until age 65. If you retire before then your healthcare costs will generally be much higher. For example, if you retire five years earlier, at age 60, you can expect to pay approximately the following over your remaining lifetime:

- 56% more for healthcare expenses than if you wait until age 65 and enroll in Original Medicare plus Medigap (Plan G) plus Part D (standard benefit).

- 89% more for healthcare expenses than if you wait until age 65 and enroll in an MAPD plan.

Note that the healthcare costs prior to age 65 are the same in each scenario and reflect premium and OOP costs for a nationwide average public exchange bronze plan with no assumed Premium Tax Credits.12

Financial impact of retiring later

Conversely, delaying retirement allows retirees to boost retirement savings and continue earning income and employer-sponsored benefits, including healthcare. This can also mean significant healthcare cost savings. For example, if you retire five years after turning age 65 (at age 70), you can expect to pay approximately the following over your remaining lifetime:

- 29% less for healthcare expenses than if you retired at age 65 and are enrolled in Original Medicare plus Medigap (Plan G) plus Part D (standard benefit).

- 30% less for healthcare expenses than if you retired at age 65 and enrolled in an MAPD plan.

Taking your health into consideration

Out-of-pocket costs for healthcare are an important part of retirement planning, and how much you will spend depends on a variety of health factors:

- Your current health status, including heart problems, arthritis, and other chronic or recurring ailments.

- Risk factors that could affect your future health status, such as tobacco use or high blood pressure.

- The level of financial risk that you are willing to take on (or withstand) by trading off lower premiums for higher deductibles and out-of-pocket costs.

Retirees with above-average health

Healthier retirees (representing the average of the lowest-cost third of Medicare beneficiaries) can expect to spend approximately the following over their remaining lifetime:

- 11% less on healthcare costs for Original Medicare plus Medigap (Plan G) plus Part D (standard benefit)

- 24% less on healthcare costs for an MAPD plan

Retirees with below-average health

Retirees with below-average health (representing the average of the highest-cost third of Medicare beneficiaries) can expect to spend approximately the following over their remaining lifetime:

- 9% more on healthcare costs for Original Medicare plus Medigap (Plan G) plus Part D (standard benefit)

- 39% more on healthcare costs for an MAPD plan

Even if you don’t have any current health issues, it is important to consider that your health status can change rapidly. There is great potential for considerable healthcare spending in the later years of life, especially if you have a chronic condition or an acute episode such as a heart attack or stroke. If you have health issues or are at risk for developing health issues, consider addressing this potential risk by budgeting for a below-average health status in retirement.

Life span considerations

While you can’t control your life span, you should plan for it. A range of plus or minus five years in life span can increase or lower retirement healthcare costs significantly. Under either plan option:

- Living five years longer increases the amount you spend by approximately 42%

- Living five years less reduces the amount you spend by approximately 32%

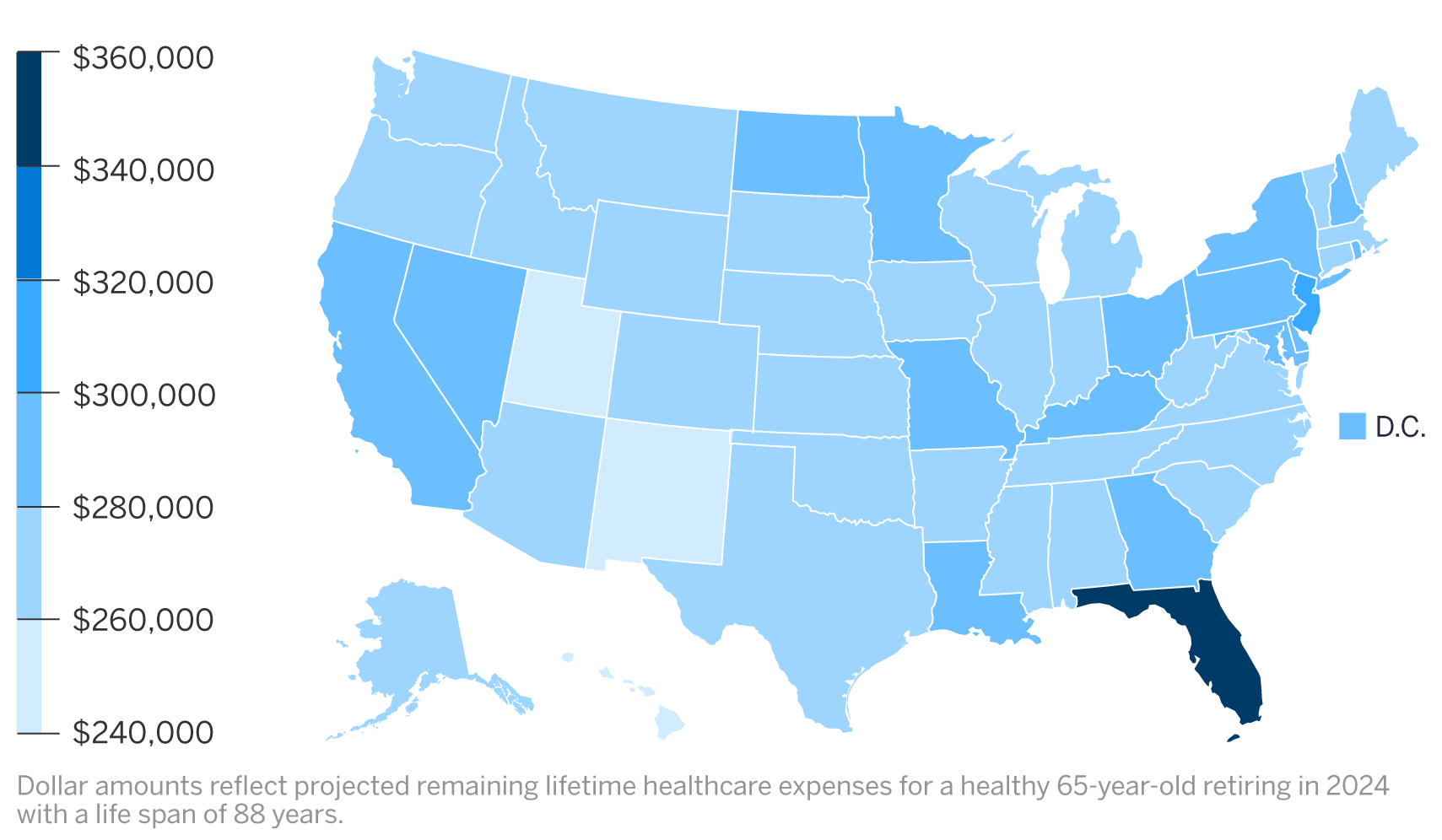

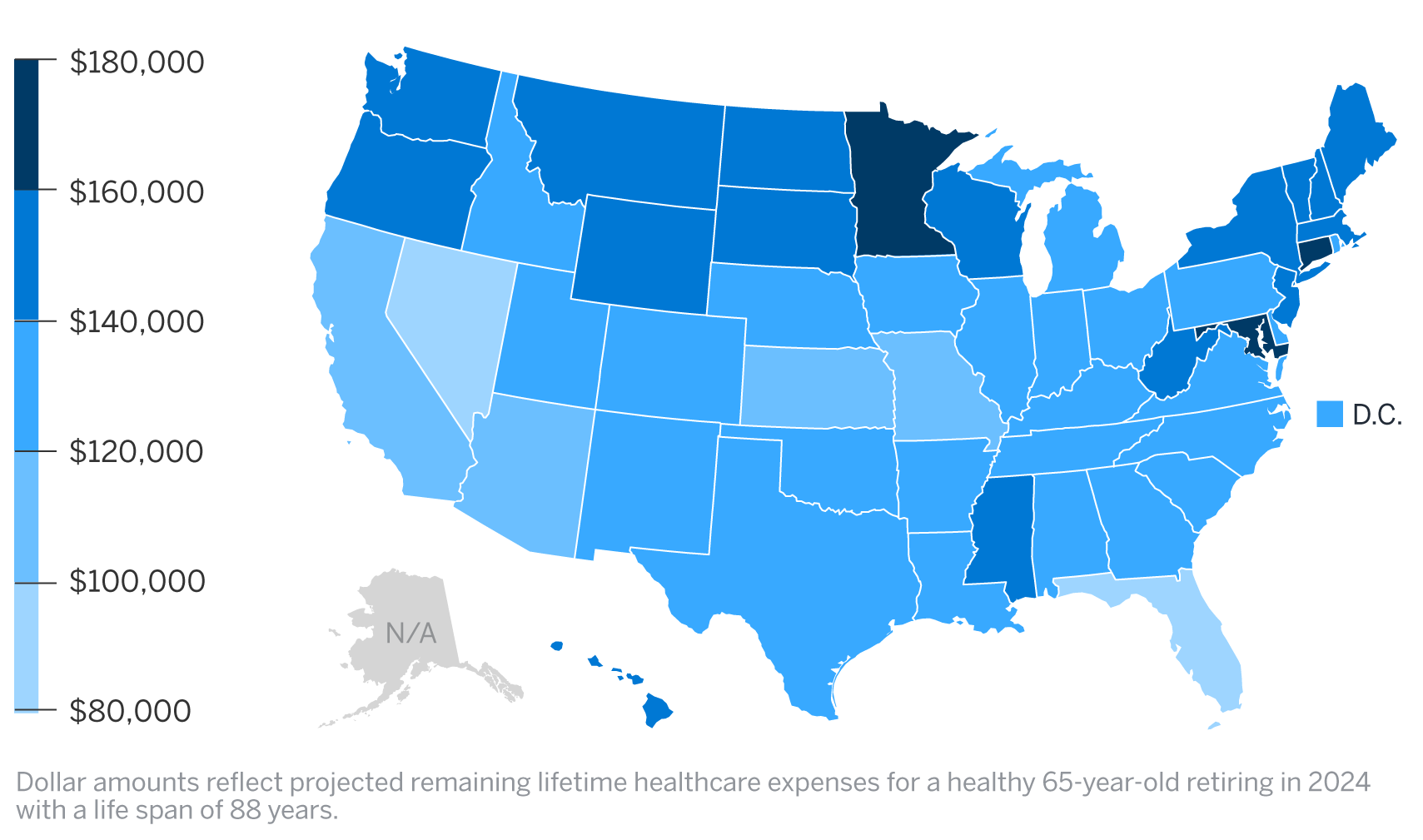

Cost variation by state

When it comes to the amount you will pay for healthcare in retirement, where you live can also be a significant factor. Although Original Medicare has standardized costs that are the same in each state, the cost of Medicare Advantage, Medigap, and Part D plans can vary greatly by state. The maps in Figures 7 and 8 show which states have higher, lower, and average costs for each pathway: for Original Medicare plus Medigap plus Part D, and for Medicare Advantage plus Part D, respectively.

Figure 7: Total spend by state – original Medicare plus Medigap Plan G plus Part D

Figure 8: Total spend by state – Medicare Advantage plus Part D (MAPD)

Summary

Healthcare expenses are an important, and sometimes overlooked, component of overall retirement planning. Start by asking yourself the following questions, and even discuss some of them with your healthcare and financial advisors:

- What is my health status (average, above average, or below average), and will that health status change over time? What can I do to affect my health status now and in the future?

- At what age am I going to retire?

- At what age am I going to enroll in Medicare, and what other types of coverage will I need?

- Do my healthcare providers participate in Medicare Advantage plans? If not, am I willing to switch providers to access reduced premiums with Medicare Advantage?

- Do I want to pay higher premiums for the freedom to see any healthcare provider I choose, or am I willing to limit my choices to in-network providers to pay lower premiums?

- Do I want to spend less money on my retirement healthcare plan monthly premiums and take on more risk for out-of-pocket expenses?

- Where will I live in my retirement years, and how will it affect my health costs?

- How should I change my retirement savings strategy to pay for the retirement healthcare plan of my choice?

By taking a realistic look at your health status and healthcare expenses as part of your overall retirement plan, and budgeting accordingly, you position yourself to enjoy a less stressful, financially healthier retirement.

Sources and assumptions

Projected costs have been calculated using the following assumptions:

- Projected costs are based on the Milliman Health Cost Guidelines™ and premium information obtained from the Centers for Medicare and Medicaid Services (CMS). Premiums prior to age 65 are sourced from HIX Compare, a program of the Robert Wood Johnson Foundation,13 and reflect a weighted average of all individual Bronze plans, based on projected 2024 enrollment.14

- Projected costs include both premiums and out-of-pocket expenses for the medical and prescription drug plans and benefits outlined under each option, limited to Medicare-covered medical costs and Part D-covered drug spending.

- Although MAPD OOP spending often includes supplemental benefits—dental, vision, hearing, over-the-counter (OTC) drugs, etc.—we have excluded the estimated value of these benefits to provide a closer parallel between the MAPD and Medigap pathways presented.

- The health status of the retiree is assumed to be average for their entire life span. This average is based on a typical commercially insured population in the Milliman Health Cost Guidelines.

- Expected life span for a current 65-year-old male and female is based on the 50th percentile using the PubG-2010 mortality table15 for general populations with mortality improvement scale MP-2021, adjusted for 2024 by the IRS.16

- To calculate increasing healthcare costs over time, Milliman estimates a future medical trend of 4.9% annually over the next 25 years. This estimate is derived using long-term economic and medical assumptions based on the Getzen-SOA trend model17 and Milliman research.

- Aging trend is also included, in addition to medical trend, where applicable (i.e., out-of-pocket expenses are generally expected to be higher for older retirees).

- For calculations of present values in today’s dollars (i.e., needed savings net of taxes), an investment return of 3.0% per year is used.

Limitations and qualifications statement

The information contained in this report has been prepared by Milliman for the purpose of retirement planning. The data and information presented may not be appropriate for any other purpose.

Any distribution of the information should be in its entirety. Any user of this report must possess a certain level of expertise in actuarial science and healthcare modeling so as not to misinterpret the information presented.

The projection of retiree healthcare costs is a complicated exercise, and actual results will vary from projections for a variety of reasons, including but not limited to changes in the following key factors:

- Laws, regulations, and rules governing healthcare plans in the United States at the federal and state levels, such as changes to the Medicare eligibility age and state Medicaid eligibility requirements

- Market forces that impact healthcare costs and plans that are available to retirees

- Changes in health status of retirees

- External shocks, such as epidemics or trends in new diseases

All of these factors may have a material effect on retiree healthcare costs. Thus, it is important to continually monitor all of the factors influencing healthcare costs and modify projections as needed.

Although the IRA enacts further changes to Medicare Part D in 2025 and beyond, no further explicit adjustments were made in the development of the projected costs in this report. It is still unclear how carriers and pharmaceutical manufacturers will react to the IRA.18 They will certainly be looking for ways to mitigate the increased plan liability, and beneficiaries may see changes to the costs of certain drugs, adjusted formularies, fewer plan options, and increased premiums as a result.

Milliman makes no representations or warranties regarding the contents of this report to parties that receive this report. Parties are instructed that they are to place no reliance upon this report prepared by Milliman that would result in the creation of any duty or liability under any theory of law by Milliman or its employees. Parties receiving this report must rely upon their own experts in drawing conclusions about the premium rates, out-of-pocket costs, trend rates, and other assumptions.

Milliman has developed certain models to estimate the values included in this report. The intent of the models was to estimate future expected premiums and out-of-pocket claims costs. We have reviewed the models, including their inputs, calculations, and outputs, for consistency, reasonableness, and appropriateness to the intended purpose and in compliance with generally accepted actuarial practice and relevant actuarial standards of practice (ASOP).

The models rely on data and information as input to the models. We have relied upon certain data and information (as described above) for this purpose and accepted it without audit. To the extent that the data and information provided is not accurate, or is not complete, the values provided in this report may likewise be inaccurate or incomplete.

The models, including all input, calculations, and output, may not be appropriate for any other purpose.

We performed a limited review of the data used directly in our analysis for reasonableness and consistency and have not found material defects in the data. If there are material defects in the data, it is possible that they would be uncovered by a detailed, systematic review and comparison of the data to search for data values that are questionable or for relationships that are materially inconsistent. Such a review was beyond the scope of our assignment.

Guidelines issued by the American Academy of Actuaries require actuaries to include their professional qualifications in all actuarial communications. The authors of this report, who are credentialed actuaries, are members of the American Academy of Actuaries and meet the qualification standards for performing the analyses contained herein.

1 For purposes of this article, a couple is defined as a male and female retiree.

2 Milliman White Paper. Part D redesign under the Inflation Reduction Act. Retrieved May 13, 2024, from https://www.milliman.com/en/insight/part-d-redesign-under-ira-potential-financial-ramifications.

3 CMS (October 12, 2023). 2024 Medicare Parts A & B Premiums and Deductibles. Retrieved May 13, 2024, from https://www.cms.gov/newsroom/fact-sheets/2024-medicare-parts-b-premiums-and-deductibles.

4 Medicare.gov. What Medicare covers. Retrieved May 13, 2024, from https://www.medicare.gov/what-medicare-covers.

5 Medicare.gov. Costs. Retrieved May 13, 2024, from https://www.medicare.gov/basics/costs/medicare-costs.

6 What Medicare covers, op cit.

7 Medicare.gov, Costs, op cit.

8 Medicare.gov. How to compare Medigap policies. Retrieved May 13, 2024, from https://www.medicare.gov/supplements-other-insurance/how-to-compare-medigap-policies.

9 CMS (December 2023). 2023/2024 Standard Drug Costs. Retrieved May 13, 2024, from https://cmsnationaltrainingprogram.cms.gov/sites/default/files/shared/2024%20Standard%20Drug%20Costs_FINAL508_2.pdf.

10 We excluded MA-only plans, employer group waiver plans (EGWPs), Medicare Cost plans, Medical Savings Account (MSA) plans, Medicare-Medicaid Plans (MMPs), and special needs plans (SNPs).

11 KFF (December 2023). A Snapshot of Sources of Coverage Among Medicare Beneficiaries. Retrieved May 13, 2024, from https://www.kff.org/medicare/issue-brief/a-snapshot-of-sources-of-coverage-among-medicare-beneficiaries/.

12 Internal Revenue Service (February 9, 2024). Questions and answers on the Premium Tax Credit. Retrieved on May 13, 2024, from https://www.irs.gov/affordable-care-act/individuals-and-families/questions-and-answers-on-the-premium-tax-credit.

13 HIX Compare. 2024 Individual Market Data Files. Retrieved January 30, 2024, from https://hixcompare.org/individual-markets.html.

14 CMS (November 12, 2023). Worksheet I, II, and III Data for 2024 Single Risk pool Filings. Retrieved January 3, 2024, from https://www.cms.gov/CCIIO/Resources/Data-Resources/ratereview.

15 Society of Actuaries (February 25, 2019). Pub-2010 Public Retirement Plans Mortality Tables. Retrieved May 13, 2024, from https://www.soa.org/resources/research-reports/2019/pub-2010-retirement-plans/.

16 Internal Revenue Service (August 11, 2023). 2024 Scale MP-2021 Adjusted Rates. Retrieved May 13, 2024, from https://www.irs.gov/pub/irs-tege/2024-adjusted-scale-mp-2021-rates-br.pdf .

17 Society of Actuaries (October 2023). Getzen Model of Long-Run Medical Cost Trends: Update for 2024-2034+. Retrieved May 13, 2024, from https://www.soa.org/resources/research-reports/2023/2024-getzen-model-update/.

18 Milliman White Paper (December 21, 2023). Stakeholder perspectives on the transformative IRA Part D benefit redesign. Retrieved May 13, 2024, from https://www.milliman.com/en/insight/stakeholder-perspectives-on-the-transformative-ira-part-d-benefit-redesign.