Long-term care (LTC) carriers are using wellness and aging-in-place programs to improve the wellbeing of their members. Interacting with LTC members at the correct times in their aging journey is a proactive measure that can help them age-in-place comfortably. From the typical LTC industry carrier's market perspective, the figure below illustrates member engagement journey on a typical LTC policy today.1 During the healthy and at-risk phases, the engagement level is the lowest. However, wellness intervention initiatives may be the most effective during these phases in terms of delaying or preventing future claims. How can carriers and wellness vendors get the insights they need to tailor outreach approaches for different groups? Milliman LARA can be the solution.

The Milliman LARA pre-claim risk model is a machine learning predictive model that is trained on LTC carrier data, proprietary third-party consumer and social determinants of health (SDoH) data, and LTC Curv Risk Tiers developed using Milliman lntelliScript® medical and prescription claim data.2 The experience data used to train the LARA pre-claim risk model has over 3 million life years of exposures. With this data, the LARA pre-claim risk model can generate risk scores and help identify which members may benefit from early intervention, before they reach severe stages of LTC needs. Risk scores can be generated over time (e.g., semi-annually) in order to monitor changes in a given population's risk profile and the underlying drivers of those changes. The LARA pre-claim risk model has superior predictive performance and has been carefully developed and analyzed with health equity in mind.3 We continuously strive to develop models that provide our clients with the intelligence they need to design and operate wellness programs that help their members achieve their highest levels of wellbeing.

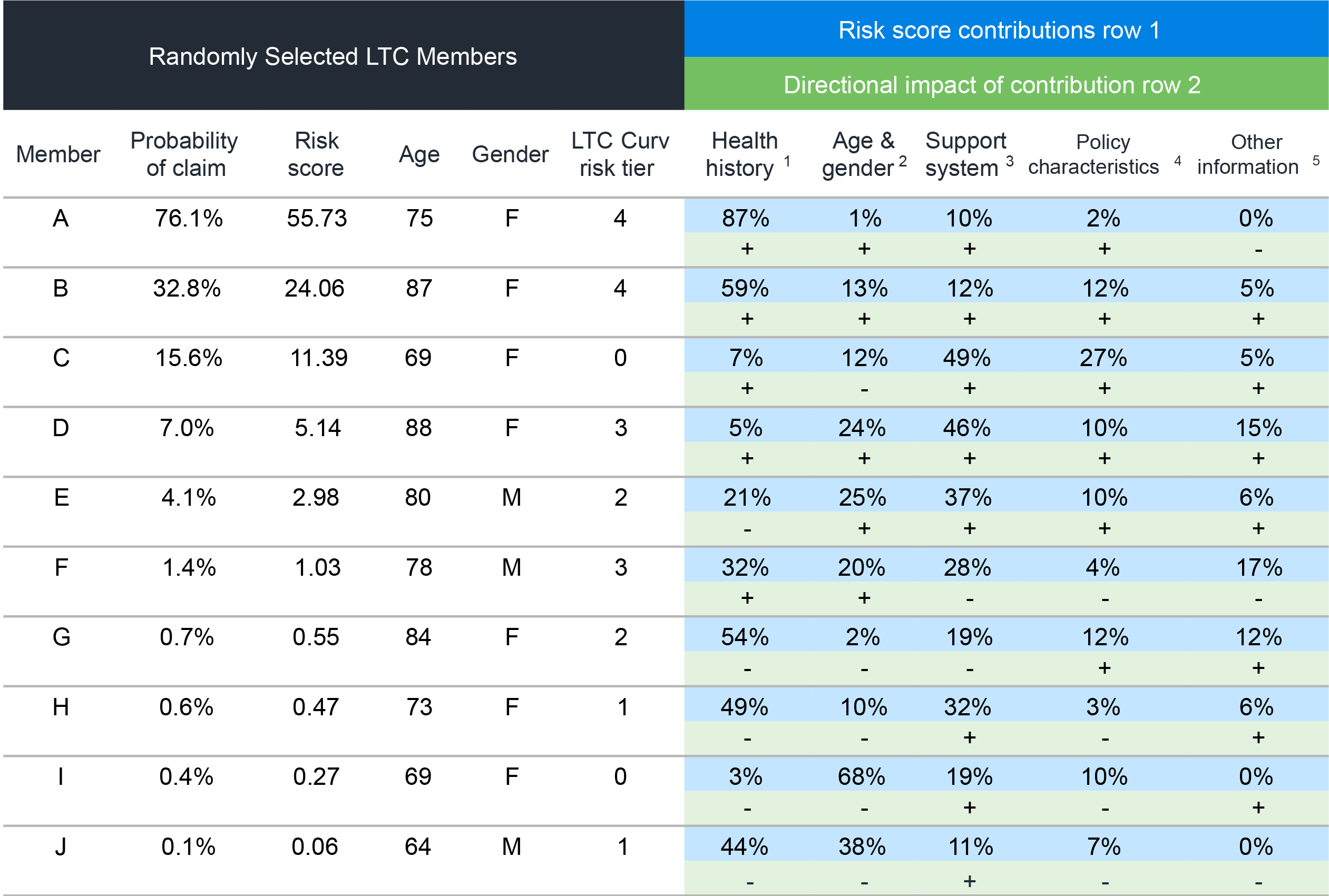

The table below provides a seriatim sample output from LARA pre-claim risk model.

1 Health history includes LTC Curv Risk Tier and previous claim information.

2 Age & gender includes information about member's attained age and gender.

3 Support system includes information about member's marital status, living condition, family condition, and more.

4 Policy characteristics includes information about member's LTC benefit such as elimination period, inflation, benefit period, and more.

5 Other information includes miscellaneous data fields such as home ownership, geographic location, and more.

- Probability of claim and risk score move in tandem, with higher values indicating the member is higher risk (i.e., higher probability of filing a claim in the next 12 months).

- LTC Curv Risk Tier are developed using medical and prescription claims data and ranges from 1 (low risk) to 4 (high risk), with 0 indicating the member's medical and prescription history was not available. Match rate depends on the quality of census data received, but it is typically greater than 90%.

- Risk score contributions and directional impact of contributions can be viewed jointly. Together they display impact on risk score from each data category and their respective direction of impact.

The figure below illustrated how a carrier or their wellness vendor could interpret and then take action from the Milliman LARA pre-claim risk model output. The sample output is at a member level, but can also be aggregated to assess the risk profile and risk drivers for entire blocks of business or sub-populations of interest.

Intervention and care management are not one-size-fits-all. To achieve high effectiveness, it is crucial to recognize the different needs of a LTC underlying population and deploy tailored care management.

This is promotional content for Milliman LARA. More information about Milliman LARA can be found on https://www.milliman.com/en/products/LARA.

1 ILTCI 2023 session: Customer Engagement – One Size Does Not Fit All

2 Milliman IntelliScript products are widely used for underwriting and segmentation in the insurance industry as a source of data and interpretation for medical claims and pharmacy histories. More information on IntelliScript can be found at https://www.rxhistories.com/.

3 https://www.milliman.com/-/media/products/lara/superior-predictive-performance-of-milliman-lara-models.ashx